Higher Education costs HOW MUCH?

Or how much I need to save for my kid's college

Hi!

It’s been a while. Like I mentioned in my last post, we had a baby girl! The last month has been part fun, part frustration, and part sleeplessness. But mostly fun.

Now that things have settled down a little in frantically-trying-to-keep-the-baby-alive phase, my wife and I have been thinking about the kid’s goals that we need start planning for.

I said in my post on why I want my Financial Independence that providing quality education for my child is one of my drivers for pursuing financial independence. I don’t know if I’ll be able to pass on an inheritance enough for her to not work for money, so the minimum I should be able to do is to provide her the education she needs to lead a fulfilled life.

For my kid’s higher education I’m making an assumption that she might go for an engineering UG degree. Of course she is free to study whatever she chooses to, as long as it’s engineering. Just kidding. But for most courses except maybe Medicine, the college fee should be comparable to that of an engineering degree.

So let’s dive in.

How much the cost is now

To be on the safe side, I picked a college which both provides quality education, and is pricey.

BITS Pilani is one of the top colleges in the country with highly regarded faculty and a great alumni network. It’s also pricey. I think it’s a decent choice to estimate college fee in the future because its fee structure is transparent. They also mention upfront that their tuition fee will increase YoY over the course of the degree, and what it will be.

Over the last 5 years, the fee in BITS Pilani has been:

That’s an average inflation of about 10%.

Side note (rant) on soaring fee

What is going on with higher education around the world? Less than 10 years ago, I completed my entire 4 year degree for a fee less than what BITS is charging today for ONE year! Okay it was a Govt college, but it had a comparable tuition fee.

Inflation is one thing, but QUADRUPLING the fee in less than 10 years?!

Okay, back to planning.

Estimating costs for the future

To keep things simple for estimations, I’ll take these assumptions:

College fee for one year today - Rs 6L

Time after which kid will join college - 18 years

Education fee inflation - 10%

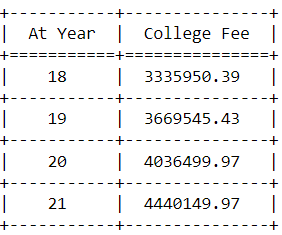

When she goes to college, the fee will be:

The total cost of college is approx Rs 1.55 Cr.

If you’d like to see the working, I’ve attached the Jupyter Notebook in the appendix.

Saving for this goal

I’ve taken a very conservative assumption of 7% return on my savings, because I don’t want to compromise on this goal at any cost. With that assumption, the investment I need comes out to around Rs 4.26L per year for 18 years.

Working, as always, is in the Jupyter notebook.

How I want to save for the goal

Since the goal is a long-term one, I can add equity to try and boost returns.

My plan is to start of with a 70:30 Equity to Debt ratio for my investments. To slowly move investments to debt as the goal gets nearer, I plan to reduce my equity exposure by around 3-4% each year. This should ensure that I have the required corpus safe by the time the fee payment comes due.

For Equity, I plan to use Index funds - Nifty 50 and Nifty Next 50 in a 1:1 ratio. N50 should provide a decent return and NN50 hopefully outperforms the N50 over the long term to compensate for the extra volatility.

For Debt, I’ll start off with PPF and the Sukanya Samriddhi Yojana. I know that these schemes have a lock in, so I can’t withdraw from them to rebalance if needed. But since I’m just starting off, I can adjust my contributions such that I can maintain the equity to debt ratio without withdrawing from funds. As the corpus gets larger, I’ll think about adding a debt fund for liquidity.

This is just the starting off blueprint, so I’ll make adjustments in the future as and when I need to. If there’s anything interesting in those adjustments, I’ll maybe write a post about it!

Wrapping up

Taking care of a kid is a lot of work. But there’s a lot of fun in looking for their smiles and being alongside them as they learn new things. Of course I can’t be an ideal parent, I will slip up some time or the other. But hopefully I do a good job taking care of my finances, so that my kid doesn’t have to grow up too quickly worrying about how to pay for her education.

Until next time!

Appendix

Here’s the Jupyter Notebook: