Inflation - Public Enemy No. 1 for FIRE

To tame it, we must first understand it

Hi!

Inflation is one of the most important considerations when deciding the corpus required for retirement. An extended period of inflation which is higher than expected can destabilize one’s plans for retiring worry-free.

But to tame this beast, we need to understand it and factor it into our calculations.

What is inflation?

Inflation is the general increase of prices and goods over a period of time. We’ve all heard the talk from folks from the previous generation who attended college for a fee of Rs 1000, but now need to spend around Rs 10,00,000 to send their children to college. This means the money we had before is worth less today, and we need to spend more to get the same quality of goods and services we had in the past.

Impact of inflation on FIRE

Once we retire in a traditional sense, we don’t have an active income to provide for our expenses - we need to rely on our retirement nest egg. We expect that corpus to grow as our investments appreciate, but we will lose out if that growth does not keep up or exceed the rate of inflation. As costs rise, our corpus will dwindle faster than before and we might run out of money before we die. Having enough money when I’m old is one of the reasons why I want to be financially independent, so this is unacceptable to me.

To prevent this scenario, I need to be able to plan for inflation during retirement.

How to measure inflation

In an ultimate sense inflation is deeply personal. Each person has different needs, and their expenses for different categories like groceries, healthcare, entertainment, etc. vary significantly. So the best way to calculate inflation is to keep track of one’s expenses over years, and then compute inflation year-over-year. But then this still has its problems:

Expenses change as a person ages. For example, medical costs would increase in the future as I grow old and need to pop in a boatload of medicines into my body each day.

Family sizes change over time. Expenses a household has changes when kids come into the picture.

Needs change over time. A early twenty year-old might be able to get by without owning a vehicle, but as kids come into the picture and parents get older relying on public transport might not be sustainable.

I can’t be bothered to track my personal expenses. Check out this post to understand why.

The Government provides a metric which does take a aggregate view of the population’s basket of needs and calculates its inflation - The Consumer Price Index. I think this is a better approach because it is a survey, and takes into account expenses at different stages of a person’s life. I’m not significantly different in terms of my household’s expenses to others, so I can use this as a rough indicator of what inflation to expect.

Calculating past inflation

CPI numbers don’t provide the complete picture of my estimated inflation though. My income is in the top quartile of income distribution, and I live in a neighborhood where the cost of living is higher for indulging in higher quality products.

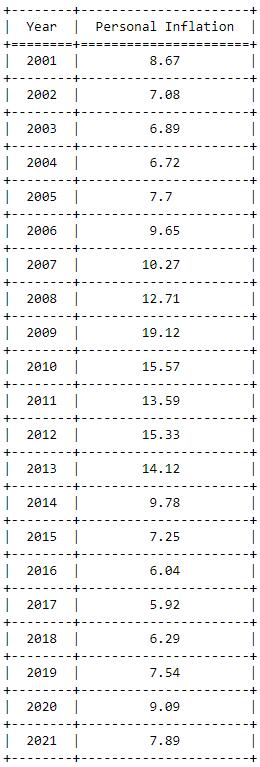

To account for that, I chose to add about 2% to the CPI values provided by the government. It’s not scientifically derived, but looking at folks close to my lifestyle who have computed their personal inflation, it looks about right. Here is the chart:

And the numbers:

My average personal inflation comes out to 9.86%.

Yikes.

This is significantly higher than the 6-7% most folks use to calculate their real returns.

For more details, check out the PDF of this Jupyter Notebook I created to compute my personal inflation:

How to manage inflation

To be honest, I don’t know yet.

This inflation number is pretty high, and there are two ways to handle it:

Increase corpus size - Even if returns are lower than inflation, I can make up using high contributions.

Decrease expenses - Try to bring down discretionary expenses to bring the personal inflation number down.

Stay tuned and subscribe to see if I can figure something out, and hopefully it helps you too!

Wrapping Up

Well, this ends on a disappointing note. My personal inflation is higher than the normal quoted number, and that will be difficult to reign in so that I can retire comfortably. But figuring out how to consume the corpus is a topic for a later time. For now, I will continue to focus on investing as much as possible.

Remember, it’s the corpus which matters in the end.